You've tried everything. Customer service ignored you. The return window closed. The store says "final sale" even though the item arrived broken. What now?

This is where a chargeback comes in. It's like a nuclear option – powerful, effective, but not without consequences. Let me walk you through when to use it, how it works, and what happens after.

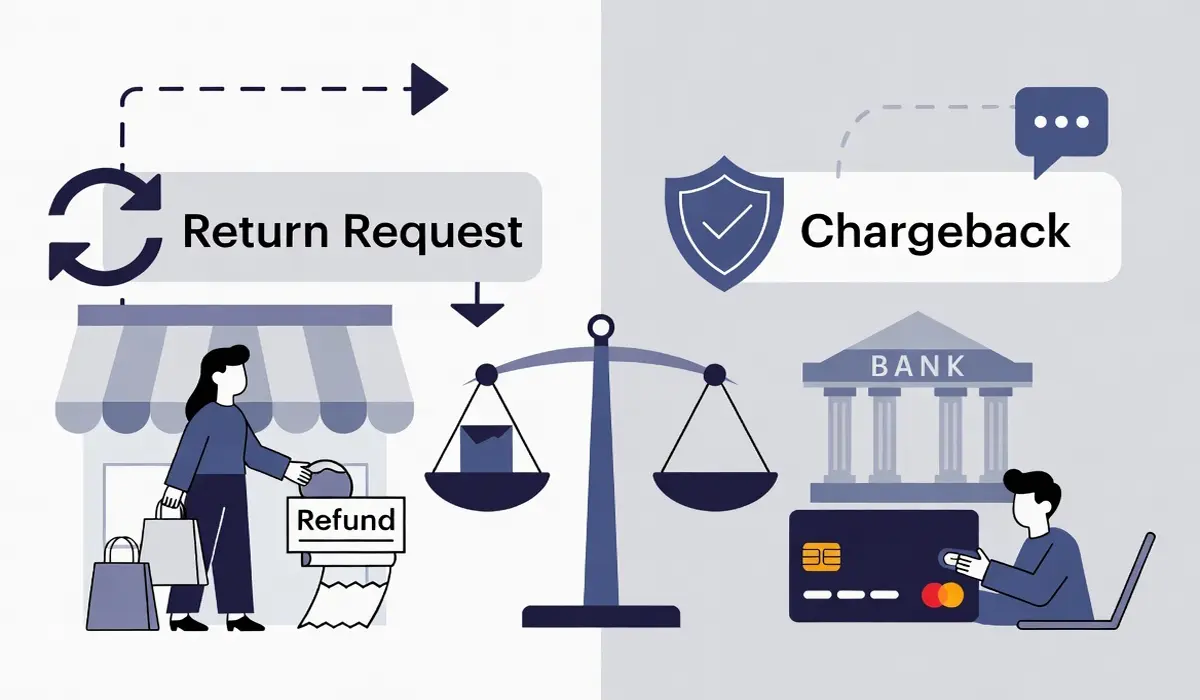

🔍 What Is a Chargeback?

A chargeback is when you ask your credit card company to reverse a transaction. The bank pulls the money back from the merchant and credits your account – pending an investigation. It's not a refund from the store; it's a dispute resolution mechanism created by Visa, Mastercard, Amex, and Discover to protect consumers.

Chargebacks exist because sometimes stores refuse to do the right thing. But they're not meant for every little problem. Banks take them seriously, and abusing chargebacks can get your account closed.

✅ When Should You File a Chargeback?

I've personally used chargebacks three times in the past decade. Each time it was justified, and I won every case. Here are legitimate reasons:

- You never received the item. Tracking shows delivered, but it's not at your door. Or the seller never shipped at all.

- The item arrived defective or damaged – but the store refuses to help. You have photos, you contacted them, they ignored you or said "final sale".

- The item is not as described. You ordered a leather jacket but got vinyl. Or a 4K TV that's actually 1080p.

- The store went out of business or is unresponsive. Their website is down, emails bounce, phone disconnected.

- Unauthorized transaction. Someone stole your card info and bought something.

In all these cases, you have a valid dispute. Banks side with cardholders about 70‑80% of the time when you provide evidence.

❌ When NOT to File a Chargeback

These are common mistakes that can backfire:

- Change of mind. You just don't like the color or it doesn't fit. That's a return, not a dispute. Filing a chargeback for change of mind is considered fraud.

- You haven't contacted the store yet. Most banks require you to try resolving with the merchant first. If you skip this step, they may deny your claim.

- You already returned the item but the refund is slow. Refunds can take 7‑14 business days. That's normal. Don't chargeback prematurely.

- You damaged the item yourself. Trying to claim it arrived broken when you dropped it – that's fraud and can get you banned from your card.

📋 The Chargeback Process – Step by Step

Here's exactly how to do it:

- Gather your evidence. Screenshots of the product page, order confirmation, tracking info, photos of the damage, email exchanges with customer service (or proof you tried to contact them).

- Call your credit card issuer. Not the store. Call the number on the back of your card. Tell them you want to dispute a charge.

- Explain clearly. "I ordered X on [date] for $Y. The item arrived damaged / never arrived / is not as described. I contacted the merchant on [dates] and they refused to help."

- Submit your evidence. They'll give you a way to upload documents – do it promptly. Missing evidence is the #1 reason disputes fail.

- Wait for a temporary credit. Most banks give you a provisional refund while they investigate (30‑90 days).

- The merchant can fight back. If they provide evidence that the item was delivered and not defective, the bank may reverse the credit. That's why your evidence is crucial.

Time limits matter: Under the Fair Credit Billing Act in the US, you generally have 60 days from the date the charge appeared on your statement. Amex and Discover sometimes give longer. Don't wait.

⚠️ The Risks: What Stores Can Do to You

I've seen people file chargebacks for stupid reasons and then regret it. Here's what can happen:

- The store bans you. Amazon, eBay, Target, and many others will close your account permanently if you file a chargeback – even if you win. They see it as a breach of their terms.

- Your credit card company might flag you. Too many chargebacks (even legitimate ones) can raise red flags, leading to account review or closure.

- The store can send you to collections. If they prove the chargeback was invalid, they can re‑bill you and send unpaid debts to collections. This affects your credit score.

- Legal action (rare). For large amounts, some merchants sue. Very rare for consumer purchases under $1000, but possible.

So think of a chargeback as a last resort – not your first move.

🤝 Alternatives Before You Chargeback

Try these first – they're less risky and often work:

- Email the CEO or executive team. Seriously. Emails like "firstname.lastname@company.com" or "jeff@amazon.com" sometimes get forwarded to a special customer support team that actually helps.

- File a complaint with the Better Business Bureau (BBB). Many stores respond to BBB complaints because they care about their rating.

- Use PayPal's dispute resolution. If you paid via PayPal, their process is easier than a chargeback and doesn't risk your credit card account.

- Post on social media (publicly). A tweet @WalmartSupport with a photo of your damaged item often gets a response within hours. Companies hate public shaming.

If none of that works – then yes, file the chargeback. Just be prepared to possibly shop elsewhere afterward.